I am absolutely no expert on Iran or international relations more generally. I happen to hold a theory, for whatever it might be worth. I think that the Iranian regime is hoping that the current war will cause a real economic crisis in the US–not a modest uptick in our inflation rate, but a serious recession.

For the Iranian leaders, a crisis would have two major advantages. First, once the American public believes that tangling with Iran can cause a recession, that would deter future US attacks. Second, once we’re in crisis, the Iranian regime may be able to get substantial cash or put pressure on Israel at the negotiating table.

They may be surprised (as I am) that a recession has not begun so far for the USA. (Other countries are already in serious pain.) But they are betting that the US will hit a recession before they lose power.

If this theory is true, then we would expect repeated news stories about negotiations (offers, counteroffers, boasts, and promises), yet no real progress. All statements about a pending “deal” would be meaningless.

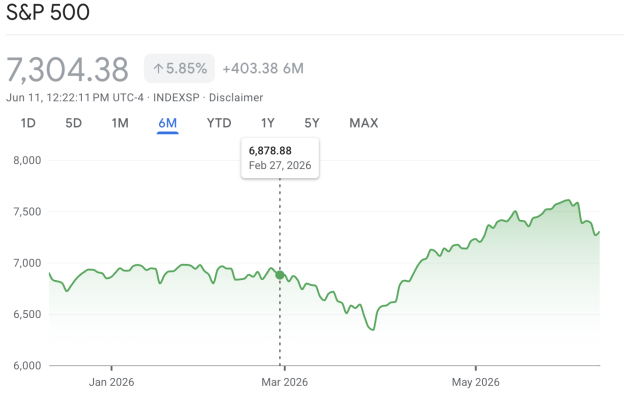

If I were an investor who made independent decisions about stocks, then my prediction would have encouraged me to get out of the market early in the war. In that case, I would have missed a 16 percent increase in the S&P between the first day of bombing and June 1–a lot of profit. Even today, the market is well above where it was on Feb. 28.

On an hourly basis, the markets have risen when either combatant suggests that a deal is on the table but have fallen whenever either side acts aggressively. From my perspective, these moves are irrational because no such news has any meaning. But again, my superior wisdom would have prevented me from earning a 16% return if I were an independent investor.

For me, the interesting question is how to think about the predictive power of markets. Millions of decision-makers who have the means to obtain specialized information and the motivation to focus on reality should make better decisions than any individual. In this case, investors have been right, and I have been wrong.

Yet I suspect that many of those investors expect a crisis to hit, or at least they view it as a risk. One explanation for their behavior is rational but short-term thinking. Even if we treat any statement from Donald Trump as hot air, it is also reasonable to predict that the market will rise immediately after he says something optimistic. So it is rational to bet on the short-term gain.

Another explanation is that masses of investors are being misled by mistaken premises, including the assumption that the two parties are motivated to negotiate and that the US side is competent.

Friedrich Hayek made a powerful case for markets, but his theory would not rule out systematic bias in a situation like this. He argues that the world at large is too complex for anyone to model it, yet alone predict it. No one knows what will happen. However, markets typically function because actors need not predict the future state of the society or the world. If you own a business, you must only predict the costs of your inputs and the willingness of consumers to pay for your products. External events like wars and elections may affect those variables a bit, but usually you can make predictions by knowing your own market. Such choices aggregate to produce prices and market conditions.

When the critical variable is a non-economic event like a war, then large numbers of investment decisions do not reflect such local knowledge. Like surveys, markets simply aggregate what lots of people believe about the world despite their cognitive, informational, and motivational limitations and biases. And in this case, the demographic traits of many investors (based in the US and the global north, familiar with business, but unaccustomed to war) may make them systematically biased to trust Donald Trump to resolve a problem that he cannot come close to managing.

See also: how markets “think” about politics; The truth in Hayek.